The home insurance market shifted meaningfully in 2025. After several years of steep premium increases and capacity constraints, the industry showed early signs of stabilization as carriers regained profitability and cautiously expanded availability in some regions. Still, premiums remain historically high, climate risks continue to intensify, and homeowners are taking on more financial responsibility through higher deductibles and stricter property-level underwriting.

This report draws on Matic’s proprietary data and industry research to review the key trends that shaped 2025. It also offers a forward-looking perspective on how insurance may impact consumers and the housing market in 2026.

Key 2025 home insurance trends

Premium growth slows, but affordability challenges continue

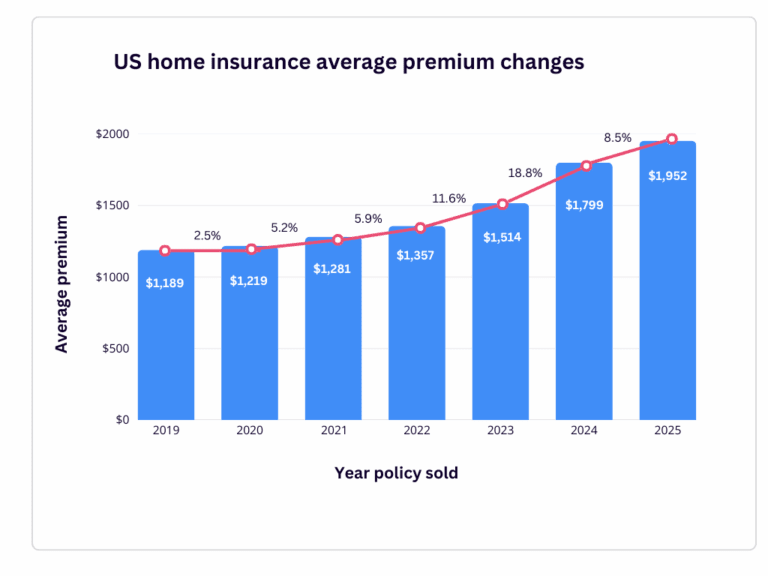

Following several years of aggressive rate increases, home insurance premium growth began to slow in 2025. As of December, Matic data shows the average premium for a new policy reached $1,952, up 8.5% year over year — a notable shift from the 18% jump seen between 2023 and 2024 and the 12% increase the year before. This moderation was driven by several factors, including carriers achieving rate adequacy after long-delayed rate increase approvals, slowing inflation, improved catastrophe risk management, and the growing use of technology to strengthen underwriting. Favorable weather patterns also helped; a third quarter without major catastrophic events gave carriers a window to stabilize reserves.

Even with this improvement, the rate of growth still far exceeds the average 3-5% increases seen before 2022, and premiums remain at an all-time high. Nationally, the uncertainty of severe weather events continues to drive elevated costs and affect home affordability. It’s estimated that insurance now accounts for 9% of the typical homeowner’s monthly mortgage payment — the highest share ever recorded. This trend has direct implications on borrowers’ ability to qualify for mortgages and to afford ongoing payments once they are homeowners. Mortgage lenders echo this sentiment, with 64% of those surveyed by Matic experiencing issues with home insurance either frequently or somewhat frequently over the last year.*

These conditions are also beginning to influence the overall housing ecosystem. In high-risk areas, the cost and availability of home insurance are beginning to influence home values and suppress demand. Since 2018, rising premiums and local risk factors have reduced home values by roughly $20,500 in the top 25% of homes most exposed to catastrophic hurricanes and wildfires — and by $43,900 in the top 10%. Homeowners in these regions are increasingly stuck: they may struggle to find or afford a policy, and if they choose to sell, they often face uncertain property values that make it difficult to move without taking increased financial risk.

Deductibles rise and roof standards tighten as insurers refine risk

In 2025, the insurance industry continued to refine its approach to risk — both by shifting more costs to homeowners and by adopting more granular, property-level analysis. The average deductible rose 22% this year, up from 15% in 2024. A higher deductible typically translates to lower premiums, which helps with affordability issues for monthly payments, but also translates to a higher out-of-pocket cost when a claim occurs. It’s likely that deductibles will continue to increase to adequately reflect today’s repair and replacement costs, as they catch up to property values that have skyrocketed in recent years.

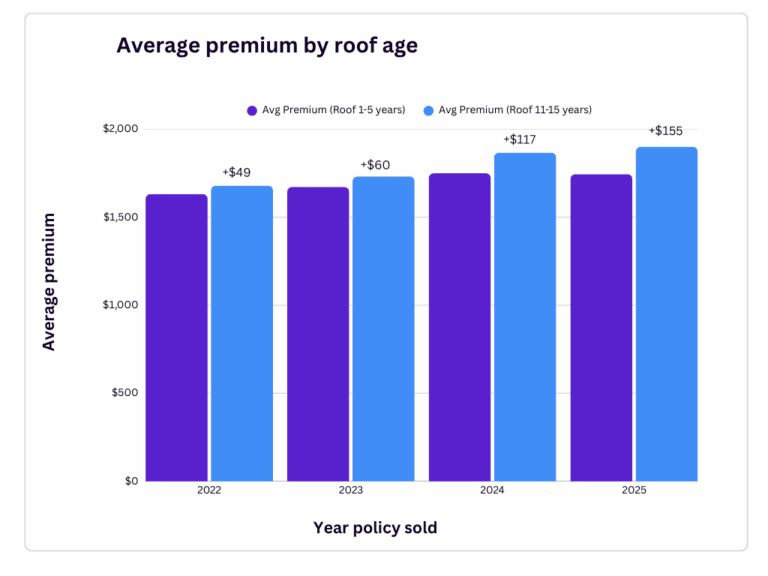

At the same time, carriers have become far more granular in assessing property-specific risk, with roof age emerging as one of the most influential factors in underwriting. In 2024, U.S. roof claims costs reached nearly $31 billion — up about 30% since 2022 — pushing insurers to scrutinize roof condition more closely.

Matic’s year-end data shows that the premium gap between newer roofs and those 11–15 years old has widened consistently since 2022. In 2022, the difference between homes with roofs under five years old and those 11–15 years old was $49. By 2025, that gap had grown to $155. This shift highlights how much weight roof age now carries in pricing, even before a roof is considered “old” by underwriting standards.

To manage this risk more effectively, carriers are accelerating their use of advanced inspection technologies, including satellite imagery, drone assessments, and AI-driven tools. These capabilities allow insurers to evaluate roof condition with greater accuracy, catch vulnerabilities earlier, and price policies based on actual property conditions rather than broad assumptions.

Insurance pricing and availability increasingly tied to geographic location

While national averages help illustrate broad trends, home insurance behaves very differently from state to state. Local climate exposure, regulatory rules within each state’s Department of Insurance, rebuilding costs, and even housing stock age all shape how carriers file rates and manage risk. That’s why homeowners in some parts of the country are experiencing dramatically sharper increases than others. The result is a widening disparity in insurance affordability and access across the U.S.

In 2025, Colorado, Texas, and Georgia saw some of the steepest rate hikes, driven by each state’s unique combination of climate risk and regulatory constraints. Colorado, for example, continues to face a “perfect storm” of risk: escalating wildfire exposure, severe convective storms, and rapidly rising reconstruction costs. As of December, homeowners purchasing a new policy in Colorado were paying $666 more than in 2024, according to Matic’s premium data.

| State | Premium Increase (%) |

|---|---|

| Georgia | +28.4% |

| Colorado | +25.7% |

| New York | +23.0% |

| Texas | +20.5% |

| Mississippi | +19.4% |

Coverage availability recovers, but California, Florida, and Texas rely on the E&S market

In 2025, access to home insurance began to improve as carriers returned to profitability. Matic data shows that by December, the number of quotes per person had risen 78% from the market’s low point in 2024. Much of this improvement came as carriers finally received approvals from state Departments of Insurance (DOIs) to implement rate increases and achieve rate adequacy after years of delays. A report from the Insurance Research Council revealed that the time it takes for regulators to approve increases has grown more than 40% since 2010.

Despite these gains, coverage availability remains uneven, with certain high-risk states continuing to experience constraints. For homeowners in high-risk regions, standard policies are often limited, costly, or unavailable, making state-backed FAIR plans and the Excess & Surplus (E&S) market critical solutions.

The E&S market has emerged as a key lifeline for homeowners who cannot secure coverage through traditional admitted carriers. Unlike standard insurers, E&S carriers are not bound by the same state regulations, allowing them to write policies in high-risk areas that admitted carriers avoid. While E&S policies typically come with higher premiums and fewer consumer protections, they provide essential coverage for properties that might otherwise remain uninsured. This trend is particularly pronounced in California, Florida, and Texas, where E&S products accounted for roughly 16% of Matic policies by December 2025, up from under 2% in 2023.

2026 Outlook

1. Climate and catastrophe risk will continue to shape the market

Climate risk will continue to drive home insurance trends in 2026. The 2025 hurricane season — the first in a decade without a major U.S. landfall — set the market on a favorable trajectory, with Swiss Re projecting premium growth to slow by 3% and AM Best revising its homeowners insurance outlook from “Negative” to “Stable.” Still, weather is unpredictable, and a major catastrophic event could quickly change premium growth, market access, and underwriting strategies.

Severe convective storms in the Midwest and Southeast have emerged as the top peril, surpassing hurricanes and coastal flooding in immediate risk. By September 2025, these storms had already caused $42 billion in insured losses, and industry leaders expect this trend to continue. In fact, 87% of insurance executives report significant or moderate concern about future losses from severe convective storms. Homeowners in regions prone to wind, hail, wildfires, or flooding face the greatest uncertainty in both costs and coverage.

2. Affordability and access challenges will fuel attempts at reform

Even with a generally more positive outlook for 2026, high insurance costs are likely here to stay. Housing affordability will remain strained, especially with mortgage rates expected to stay above 6% through 2026. And while coverage availability is improving, it’s still much lower than historical norms. High-risk ZIP codes and states like California, Florida, and Texas will likely continue to face the biggest challenges, keeping the Excess & Surplus (E&S) market a critical solution.

These pressures are pushing more conversations around consumer protections and reform. The National Flood Insurance Program (NFIP) is up for reauthorization in January, prompting broader discussions about overhauling the program. At the same time, consumer advocates — including a recent petition from Consumer Reports — are calling for stronger policyholder protections. All signs point to access and affordability remaining front-and-center issues for regulators, policymakers, and insurers in the year ahead.

3. AI and technology integration will become core to insurance operations

AI and advanced technology are poised to play an even more central role in home insurance in 2026. Carriers are expanding their use of satellite imagery, drone inspections, and predictive analytics to evaluate property-specific risks, while also incorporating localized weather risk data and catastrophe modeling to anticipate losses and refine pricing. These tools support more precise underwriting and open the door to flexible coverage structures that better match a home’s actual risk profile. Carriers may also begin leaning more heavily on AI to interact with consumers online, moving beyond traditional chatbots toward systems capable of making decisions and completing tasks autonomously.

AI is also reshaping how homeowners shop for insurance. Large language models (LLMs) like ChatGPT help consumers better understand their coverage needs and make more informed decisions — potentially shifting demand toward more customized coverage instead of default recommendations. Adoption of LLMs is expected to accelerate in 2026, with some experts predicting that up to half of U.S. consumers will use AI tools to research or shop for insurance policies.

4. Proactive risk management will be a focus

Proactive risk mitigation is expected to become an even larger focus in 2026 as carriers look for ways to prevent escalating loss costs. Programs like Nationwide’s Ting, which monitors electrical systems to prevent fires, and SageSure’s roof shingle reinforcement initiative demonstrate the industry’s approach of making small upfront investments aimed at reducing the likelihood and severity of future claims. Going forward, more insurers may explore similar programs, offer premium incentives for documented mitigation efforts, and integrate property-level risk data into underwriting decisions.